State of O’Keefe Stevens Advisory: Q3 2024 Update

Written by Justin Stevens

As we conclude the third quarter of 2024, we’re pleased to share several important updates with you. This has been a year of growth and innovation at O’Keefe Stevens Advisory. We are proud to have been recognized on the 2024 Inc. 5000 list at #4,570, as well as in the Rochester Top 100. While these accolades are nice to share, the real satisfaction comes from operating a “well-oiled” machine and continue to help more people save, invest, and retire with confidence.

One of our major internal achievements this quarter was surpassing $400M in Assets Under Management, ending the third quarter above $420M. This growth reflects your continued trust in us and the success of our long-term investment strategies. Of course, what matters most to you, our clients, is the steady progress in your portfolios, reinforcing the importance of staying focused on long-term goals despite short-term market fluctuations.

We’ve made several operational improvements to better serve you. We welcomed Sue Tsakos as our new Executive Assistant to Peter O’Keefe. Many of you will have an opportunity to meet and interact with Sue in the coming months as Peter plans to host a few client update lunches in the Buffalo area. Additionally, Dominick implemented the Orion Eclipse trading system, streamlining our processes and improving our portfolio management service. Peter and I also rolled out a formal succession plan and equity participation arrangement to ensure the long-term stability of our firm and the continuity of service for generations to come. While we both intend to stay active at O’Keefe Stevens Advisory for many more years, this initiative provides our longest-tenured teammates with an opportunity to grow with our business and incentivizes them to stay with us into future years.

We continue to improve our marketing efforts, adding new digital lead generation tools to increase efficiency in reaching prospective clients. We are launching an online webinar series to educate individuals on topics such as tax planning, Roth IRA conversions, and other timely financial subjects.

As we look ahead to the fourth quarter, our focus remains on enhancing the client experience, growing our team, and continuing to build on the strong foundation we’ve established. Thank you for your trust and partnership as we continue on this exciting journey.

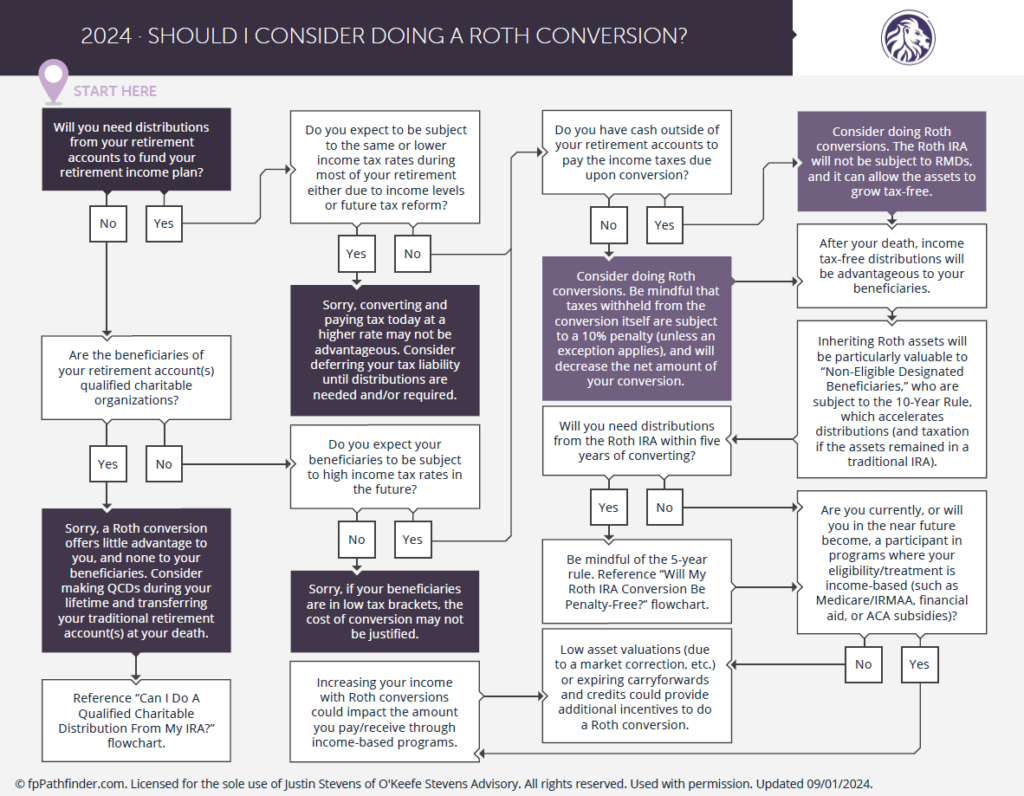

Considering Roth Conversions? Read this.

Written by Grace Stolberg

I frequently encounter the same recurring questions from clients: Am I saving enough for retirement? How can I minimize my taxes? Do I need a trust? Among these, one question clearly takes the cake as the most frequently asked question.

Should I do Roth Conversions?

The short answer:

Yes. For most retirement savers, converting Traditional Retirement Accounts to Roth will lower your total lifetime taxes paid and increase the value of the estate you leave to your heirs. If that sounds appealing, keep reading.

What is a Roth Conversion?

A Roth Conversion involves moving funds from a tax-deferred account (like a Traditional IRA or 401(k)) into a Roth IRA. The amount converted is taxed as ordinary income for that year. After paying the taxes, funds in the Roth IRA can grow tax-free.

Why Consider Roth Conversions?

If you’ve been a diligent saver and a prudent investor over the course of your career, you will have a substantial amount of savings in tax-deferred accounts. This is great! However, Traditional Retirement Plans have one problem: You also have a substantial IOU to the IRS. Large balances in tax-deferred accounts can quickly become problematic once Required Minimum Distributions (RMDs) kick in, starting between ages 73 and 75 based on your birth year. RMDs increase every year to provide the IRS with tax revenue on funds that were accumulated in tax deferred accounts. This requirement may mean you are forced to take much larger withdrawals than your actual income need. This could mean unnecessarily higher tax bills over your lifetime.

Roth Conversions, when done with proper tax planning, can help manage this pending tax problem. By converting funds to a Roth IRA, you pay taxes now, at a lower rate. This savvy maneuver works to reduce future RMDs and lower the overall tax bill on your withdrawals. A Roth conversion strategy gives you more control over your retirement income and may even eliminate RMDs if done early in your retirement years.

Key Considerations Before Converting

Understand Your Total Household Income

Roth Conversions are taxed at your effective income tax rate. As your income increases, you are required to pay a higher percentage of taxes at the Federal level (and in many states too). Therefore, it’s essential to have a clear picture of your total household income before you decide to convert. This includes any capital gains, interest, and dividend income from your portfolio. To optimize your conversion strategy, it’s best to wait until the end of the year to evaluate your full income picture. At year end, review your household income in detail, accounting for all sources and their tax implications. By identifying any additional income, such as bonuses or significant realized capital gains, you can accurately project the costs associated with Roth conversions. This detailed approach will help you avoid unexpected surprises come tax season.

Consider Future Lower-Income Years

If you’re near retirement, it’s often wise to wait until you’re fully retired to start Roth conversions. Without earned income, your taxable income will most likely be comprised of Social Security payments, any pension or annuity benefits, IRA withdrawals, and dividend and interest paid out to you during the year. This time of lower income before your RMDs begin from tax-deferred accounts, is the ideal time to convert. You will likely be in a lower tax bracket, giving you more room to convert funds at a lower cost.

Get Dollar Specific on Projected Tax Savings

A significant part of the financial planning work I do with my clients is projecting their yearly tax liability over the coming decades. When I create Retirement Income Projections for my clients, I’m able to look ahead to see what years will have lower taxable income. Then we can design a Roth Conversion strategy and project what years are the best to convert. When we do this date-specific/dollar-specific planning, you can determine a dollar value for total tax savings throughout the course of your life from choosing to do Roth Conversions. This process helps determine the optimal timing and appropriate amount of Roth Conversions for your household each year.

Do You Have Other Funds to Cover Taxes?

It’s best to have funds outside of your retirement accounts to pay the taxes on a Roth Conversion. Ideally, you should avoid withholding from the conversion amount itself. For example, if you convert $100,000 and withhold 25% for taxes, only $75,000 will make it into the Roth IRA. This automatically eliminates a quarter of your conversion from reaping the benefits of tax-free compounding. It would be better to convert $100,000 and pay the 25% tax bill from another source like a bank account or brokerage account. We recommend planning ahead to cover these taxes, so the full amount of conversion benefits from tax-free growth.

Consider all Forms of Taxes When Converting

Income taxes at the federal and state levels are not the only tax consequences when you convert to a Roth IRA. It’s important to be mindful of Medicare Premium Taxes when considering a Roth conversion. The brackets for Medicare Income-Related Monthly Adjustment Amounts are an important consideration if you are on Medicare. When evaluating Medicare premiums, the Social Security Administration looks at your taxable income from two years prior. Knowing how much you will increase your income by converting to Roth, will help avoid unnecessary taxes on your future healthcare related costs.

Impact on Your Heirs

Roth conversions are a powerful tool for lowering future tax liability and growing your wealth tax-free. However, if your income remains high throughout retirement due to pensions or other income sources, you might not experience substantial tax savings yourself. Don’t less this discourage you, though. The real benefit could be for your heirs. Under Secure Act 2.0, those inheriting a non-spouse Traditional IRA have 10 years to fully empty the account. Your beneficiary will be forced to take RMDs in years 1-9, and have the account emptied by year 10. Every dollar distributed from a Traditional IRA is taxable to them at their effective tax rate, forcing them to split their inheritance with Uncle Sam. Inherited Roth IRAs must also be emptied by the 10th year following the original owner’s death. However, your beneficiary will not have RMDs and can leave the money to grow tax-free over the 10 years. When they do take a distribution (by the end of the 10th year) they’ll pay absolutely $0 in tax on distributions. When you convert your wealth to a Roth IRA, you ensure more of your wealth goes to your loved ones rather than to the IRS.

Final Thoughts

Roth Conversions are a hot topic among retirees and financial planners. Most people today believe tax rates will be higher in the future than they are today. A Roth conversion can be a great tool to lower future tax liability and to provide your heirs with a tax-free inheritance. But you need to be prudent. Roth conversions can also come with a lot of problems if you convert your tax-deferred dollars without planning around taxes. It’s important to work with your advisor to optimize the timing and amount you convert.

A Closing Window for Estate Planning

Written by Justin Stevens

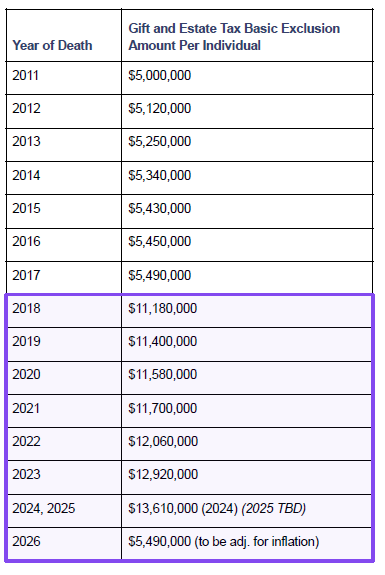

As you may know, the Tax Cuts and Jobs Act of 2017 brought about some favorable changes to estate and gift taxes. The lifetime estate and gift-tax exemption amounts were increased to $13.61 million for individuals and $27.22 million for married couples. This means that right now, you can transfer a substantial amount of wealth to your heirs without facing federal estate taxes. However, these increased exemption amounts are set to expire on January 1, 2026, and unless new legislation is passed, they will revert to approximately $7 million for individuals and $14 million for married couples.

Source: Internal Revenue Service

What does this mean for you? Essentially, we’re in a “use it or lose it” situation. If we don’t take action now, there could be a significant financial impact later. The federal estate tax rate is 40%, so the reduction in the exemption could result in a tax liability of up to $2.8 million per individual or $5.6 million per married couple. But there’s good news: the IRS has clarified that any benefits you lock in under the current exemption won’t be taken away, even after the exemption amounts drop.

This is where strategic planning becomes crucial, and there are two key strategies I’d like to highlight: lifetime and annual gifting and trust planning.

Lifetime and Annual Gifting: This is a fantastic way to transfer wealth to your loved ones while minimizing your estate’s tax exposure. By making gifts during your lifetime, you can reduce the size of your taxable estate, potentially shielding it from future estate taxes. Additionally, the IRS allows you to give up to $18,000 per recipient ($36,000 for married couples) each year without it counting against your lifetime exemption. These annual gifts may seem small, but they can add up over time and significantly reduce the taxable value of your estate. Plus, you can also make direct payments for tuition or medical expenses, which do not count towards the gift-tax limit at all.

Trust Planning: Establishing trusts can provide another layer of protection for your estate. Trusts allow you to transfer assets in a controlled manner, often with significant tax benefits. By placing your assets in the right type of trust, you can ensure they grow outside of your estate, protecting them from future taxes. Trusts also offer the flexibility to manage how and when your heirs receive their inheritance, helping to preserve wealth across generations.

Now is truly the best time to consider these strategies, while the current tax laws are still in place. By acting now, we can help you secure a lasting financial legacy for your family. We’re here to guide you through every step of the process and ensure that your estate plan aligns with your broader financial goals.

Please don’t hesitate to reach out if you have any questions or if you’d like to discuss your options in more detail. Together, we can create a plan that maximizes your wealth and minimizes taxes, so you can enjoy peace of mind knowing your loved ones are taken care of.

In Memoriam

Written by Peter O’Keefe

It is with deep sadness and heartfelt gratitude that we remember four of our cherished clients whom we lost during the third quarter: Marion O., Ralph H., Barbara L., Frank B, and Anne L.

Each of these individuals was a long-term client of O’Keefe Stevens Advisory, and over the years, we had the privilege of not only working with them but also building meaningful relationships. They entrusted us with their financial well-being, and in turn, we came to know them as friends. Their confidence in us, their loyalty, and their belief in our mission have played a significant role in shaping the firm we are today.

We are grateful that their legacies continue, as their children and grandchildren have chosen to remain part of the O’Keefe Stevens family. Their ongoing trust is a testament to the bonds that extend beyond one generation, and we are honored to be part of that continuity.

As we reflect on the lives and legacies of Marion, Ralph, Barbara, Anne, and Frank, we extend our deepest sympathies to their families and loved ones. They will be greatly missed, but their impact will remain with us for years to come.

Disclaimer: Although we obtain information contained in our newsletter from sources we believe to be reliable, we cannot guarantee its accuracy. The opinions expressed in the newsletter are those of O’Keefe Stevens Advisory and may change without notice. The information in our newsletter may become outdated and we have no obligation to update it. The information in our newsletter is not intended to constitute individual investment advice and is not designed to meet your personal financial situation. It is provided for information purposes only and nothing herein constitutes investment, legal, accounting or tax advice, or a recommendation to buy, sell or hold a security.

Investment advisory services are offered through O’Keefe Stevens Advisory, Inc., an SEC Registered Investment Advisor.

© 2024 O’Keefe Stevens Advisory, Inc. All rights reserved. This content cannot be copied without the express written consent of O’Keefe Stevens Advisory, Inc.

No responses yet