ESOPs vs. ESPPs: Understanding the Difference and Benefits

Written by: Grace Stolberg

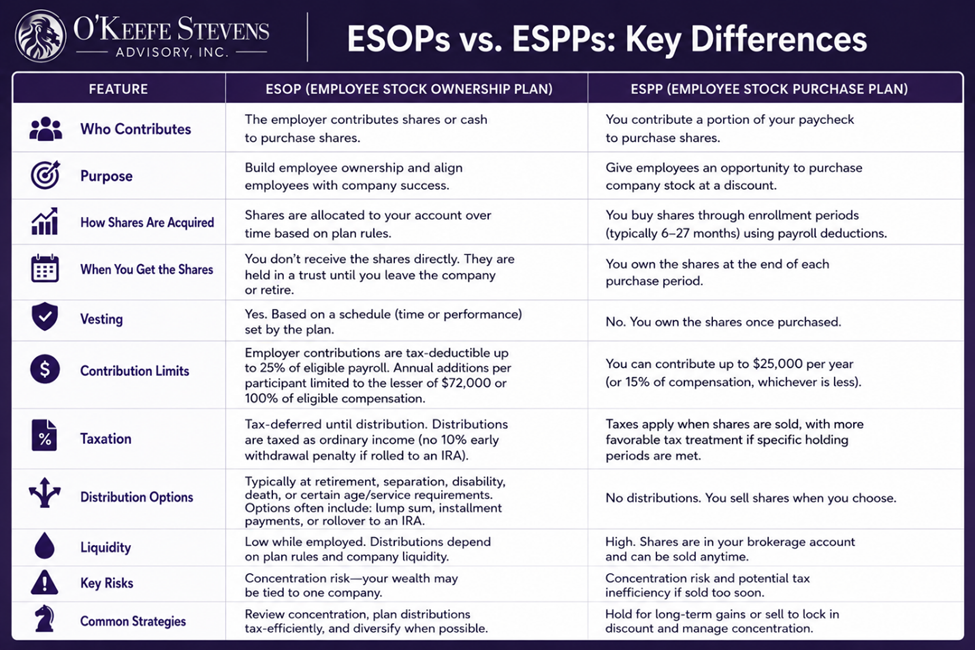

In my role as a financial advisor, I frequently hear clients using the terms ESOP and ESPP interchangeably. In reality, these plans are vastly different in terms of contributions, structure, and tax implications, and understanding what you’re participating in is crucial to ensuring you get the most out of these benefits.

Many employees participate in these programs for years without fully understanding how the shares are acquired, how distributions are taxed, or what options become available when they retire or leave their employer. I get it. These plans don’t operate like the retirement plans most people are used to, like 401(k)s or pensions, and most people have never had someone sit down with them for even 5 minutes to explain the details, tradeoffs, and planning opportunities that come along with them.

That lack of clarity can lead to unnecessary taxes, overconcentration in company stock, or missed planning opportunities over time. This article is designed to break down the basics of ESOPs and ESPPs, including how each plan works, who contributes, how taxation is handled, and what employees should know before making decisions with their shares.

What Is an ESOP?

An Employee Stock Ownership Plan (ESOP) is an employer-funded benefit that allows you to participate in company ownership. Companies typically incorporate these plans to further incentivize employees to improve corporate performance and increase the company’s value.

Instead of contributing your own money into the plan like you would with a 401(k), your company contributes either shares of its stock, or cash to purchase stock on your behalf over time. Those shares are not immediately made available to you, though. Typically, your shares are held in a central trust until you become vested and eventually leave the company or retire. Vesting schedules can vary as well, with some plans based on set periods of time and others tied to company or individual performance. You, as a participant, incur no tax liability until starting distributions, which can be done in a variety of ways, each with their own tax considerations.

How does an ESOP work in practice?

At the core of the plan is the ESOP trust. As briefly mentioned before, the company contributes shares of stock into the trust over time, and those shares are then allocated among eligible employees based on factors like compensation, tenure, or years of service. In some cases, the company contributes cash to the trust, which is then used to purchase company shares.

As an employee, you generally won’t receive physical shares in a brokerage account right away. Instead, you’ll typically have an ESOP account that tracks how many shares have been allocated to you and what they are currently worth.

Contribution Limits

Generally, employer contributions to an ESOP are tax-deductible up to 25% of eligible payroll each year. From there, the annual additions for each individual participant cannot exceed the lower of $72,000 or 100% of the participant’s eligible compensation.

Vesting

Over time, you become vested in those shares according to the plan’s vesting schedule. Once vested — and typically once you retire or separate from the company — you become eligible to receive distributions from the plan.

At that point, employees are faced with an important decision: to keep or to sell. Holding the shares may provide continued upside if the company performs well, but it can also create significant concentration risk depending on the total benefit in relation to your broader financial picture. This decision should be reviewed in relation to your near and long-term financial plan. Don’t have a plan? Our financial planners in Rochester, NY can help.

It’s also worth noting that ESOP trusts are not necessarily required to hold only company stock at all times. While ESOPs are primarily designed around employer stock ownership, some plans may hold cash or other investments alongside company shares depending on the plan structure and liquidity needs.

ESOP Distributions and Taxation

Employees participating in an ESOP are only taxed once distributions occur. There’s no tax owed by the employees when shares are contributed by the employer, nor when shares vest. Taxes are fully deferred until distributions occur, much like a traditional pre-tax retirement account. This is a powerful feature of the plan, as you can participate in years of growth and dividends without incurring taxes.

Once you take a distribution, the IRS is ready to collect. Typically, distributions can begin after you’ve retired or separated from the company, become disabled, have met a certain age or service requirement, or at death. Most plans do not allow distributions if you’re under age 59 ½. If you make a distribution before the allowed age, you’ll face a 10% penalty based on the total distribution – that’s on top of taxes.

Your ESOP’s plan document will outline the specific rules and options for distributions, but typically, you either can elect to rollover your benefit to an IRA, take a full lump-sum distribution, or spread the distribution over a set time period, typically 5 years. It’s also worth noting that any existing ESOP balance in your name will be included when calculating your Required Minimum Distributions if you’ve reached your Required Beginning Date (age 73 if born between 1951-1959, age 75 if born in 1960 or later).

Distributions must begin no later than by year-end, one year after the qualifying event (retirement, reaching a certain age, etc.), or after 6 years of leaving the company for reasons like termination or resignation.

The amount of an employee’s ESOP distribution is based on three factors:

- Number of shares allocated to the participant

- Value per share at time of distribution

- Whether the participant is fully or partially vested in their ESOP account at the time of the distribution – if you’re not fully vested, you will receive only the vested portion of the distribution.

Option 1: Lump-Sum Distribution

Most plans will typically allow for a simple lump-sum payout in cash. Some plans will allow for a distribution in stock, followed by their immediate repurchase of your stock, effectively translating to a cash payout. In this case, the total value of the distribution is taxable to you that year as ordinary income.

Option 2: Substantially Equal Payments Over Time

If you want to receive your benefits from the ESOP in the near term but want to avoid taking the tax hit all in one year, you may elect to be paid out over a set period of time, typically 5 years. The value of your ESOP, upon electing this distribution option, will be divided into substantially equal annual payments.

Each payment is then taxed as ordinary income in the year in which it is paid.

Option 3: Rollover to IRA

If for any reason, you do not want or need to distribute your ESOP at retirement or separation, there’s an important option available to continue the deferral of taxes. Upon leaving the company or becoming eligible for a distribution, you can elect to rollover your ESOP balance to an IRA, much like rolling your 401(k) or 403(b) to an IRA.

If you elect this option, the transfer should occur as a direct rollover, instead of a 60-day rollover, to avoid a potential tax penalty. This can be very attractive for employees who do not have an immediate need to access funds in retirement.

Another important planning opportunity to note with ESOPs involves something called Net Unrealized Appreciation (NUA).

Option 4: Company Stock Distribution and NUA (Net Unrealized Appreciation)

Instead of rolling your ESOP into an IRA or cashing out, your plan may allow for distributions in company stock. In this case, your shares would be transferred to a brokerage account. The original cost basis of the shares is taxed as ordinary income upon distribution, while future appreciation may qualify for long-term capital gains treatment when sold if held for more than 1 year after distribution.

For people with highly appreciated employer stock, this can create substantial tax savings compared to rolling everything into an IRA and eventually withdrawing it as fully taxable ordinary income.

However, NUA strategies are highly specific and need to be evaluated carefully. In many cases, rolling the assets into an IRA still makes more sense depending on age, diversification needs, tax brackets, and long-term goals.

Now onto the not-so-similar plan, the ESPP.

What Is an ESPP?

An Employee Stock Purchase Plan (ESPP) works quite differently than an ESOP. One helpful hint, the words “employee purchase” are right in the name.

Instead of the employer contributing shares like in an ESOP, employees contribute their own earnings through payroll deductions to purchase company stock, often at a significant discount to the current fair market value.

Most ESPPs allow employees to buy shares at up to a 15% discount from the market value. If you work for a company that has publicly traded stock, this means that while others are purchasing your company stock at the current market price, you’re able to purchase the same stock at a much cheaper price. If you have confidence in your company’s growth potential or ongoing success, you should take advantage of this valuable opportunity.

Some plans also include a “lookback provision,” which allows the purchase price to be based on the lower stock price between the beginning and end of the offering period. This can significantly increase the effective discount and creates a very attractive opportunity to participate in the potential growth of your company.

How does an ESPP work in practice?

Employees participating in an ESPP elect to have a portion of their paycheck withheld throughout the year, just like you would elect to have a portion of your paycheck go to your 401(k) or an HSA. Those payroll deductions accumulate over a set “offering period,” and at the end of that period, the funds are automatically used to purchase company stock on the employee’s behalf at the plan’s discounted price.

Offering periods vary by company, but many plans operate on 6-month or 12-month cycles. For example, if you elected to contribute 10% of your paycheck to the ESPP and accumulated $6,000 over the offering period, that money would then be used to purchase company shares at the discounted purchase price established by the plan.

Unlike an ESOP, where shares are typically held inside a trust until retirement or separation from service, ESPP shares are usually deposited directly into a brokerage account in your name shortly after purchase. Once the shares are purchased, you generally have full control over them. You can hold the shares, sell them immediately, or continue building a larger position over time.

Contribution Limits

While ESPPs can be incredibly valuable, there are limits on how much stock employees can purchase through the plan each year. Under current IRS rules, employees can purchase up to $25,000 worth of stock annually based on the stock’s value at the beginning of the offering period. To clarify, the $25,000 limit is based on the actual market value of the shares when granted, not on the discounted purchase price.

Many companies also impose their own contribution limits. For example, a company may allow employees to contribute no more than 10% or 15% of their salary into the plan, even if IRS rules would technically allow a larger contribution.

Holding vs. Selling the Shares

One of the biggest decisions employees face with an ESPP is whether to hold the stock after purchase or sell it immediately.

Some employees choose to sell the shares right away in order to lock in the discount and recognize a relatively low capital gain. Others hold the shares because they believe the company stock will continue appreciating over time.

The best decision depends on your broader financial picture, your confidence in the company, your tax situation, and how much exposure you already have to company stock.

This is especially important because many employees may already have significant exposure to their employer through salary, bonuses, RSUs, stock options, or retirement plans. Continuing to accumulate large amounts of company stock can create concentration risk, meaning too much of your financial future becomes tied to the success of one company.

Even excellent companies can go through difficult periods, which is why these decisions should always be reviewed within the context of your overall financial plan.

ESPP Taxation

This is where things can become a little confusing.

Unlike ESOPs, ESPPs are not tax-deferred retirement plans. Contributions are made with after-tax dollars, no taxes are owed on the purchase, and taxes are triggered once the shares are sold. However, how those shares are taxed depends on when you sell.

There are two primary ways ESPP sales are taxed: qualifying dispositions and disqualifying dispositions.

Disqualifying Disposition

A disqualifying disposition occurs when an employee sells the shares too quickly to qualify for preferential tax treatment. Specifically, this means selling the shares before meeting not one, but two required holding periods:

- You must hold the shares at least two years from their offering date (when you could elect to purchase that specific set of shares).

- Many plans have offering periods of 6 months, so you’d need to wait a year and a half after the purchase date to enjoy the preferential tax treatment of a Qualifying Disposition.

- You must then continue to hold your shares for at least one year from the purchase date (when the shares were purchased at the end of the offering period).

If you do not meet each of these requirements, the discount you received, or the “bargain element”, is taxed as ordinary income. Your employer will report the bargain element as compensation on your W-2, so you’ll pay taxes at your effective federal and state rates. Any profit received after selling the stock is then taxed at either short or long-term capital gains rates depending on your holding period.

For example, suppose your company stock was trading at $100 per share and you purchased it through the ESPP for $85 because of a 15% discount. If you immediately sold the shares for $100, the $15 discount would be treated as ordinary income and will show up on your W-2.

If the market price rose to $110 after 1 month of purchase and you decided to sell at that point, the $15 original discount, along with the $10 in price appreciation, would be taxed as a short-term gain (ordinary income rates).

Many employees use this strategy because they simply want to capture the discount and avoid the risk of holding too much company stock long term.

Qualifying Disposition

A qualifying disposition occurs when the required holding periods are met. In this case, a portion of the gain may qualify for the more favorable long-term capital gains tax rates instead of being fully taxed as ordinary income.

Ordinary Income Component

In most cases, the discount you originally received on the stock purchase is taxed as ordinary income at sale.

Capital Gains Component

If you’ve sold your shares at a profit, any remaining gain over the discount is taxed at the more favorable long-term capital gains rates.

For example, if your company stock was worth $100 and you purchased it through the ESPP for $85 because of a 15% discount, then later sold it for $140 after meeting the holding requirements, your total gain would be $55. Of that gain, the original $15 discount would generally be taxed as ordinary income, while the remaining $40 would be taxed as a long-term capital gain.

This can create meaningful tax savings in some situations. However, holding the shares longer also means taking on additional market risk, since the stock price could decline during the holding period. In many cases, the potential tax savings need to be weighed against the risk of remaining concentrated in a single stock.

In Conclusion

Both ESOPs and ESPPs can be tremendous wealth-building opportunities when used strategically. But without a clear understanding of the tax rules, distribution options, and risks tied to concentrated company stock, these benefits can just as easily create costly mistakes, unnecessary taxes, and an unhealthy dependence on a single company for your financial future. The key is understanding how these plans fit into your broader financial life and making decisions intentionally, not reactively.

At O’Keefe Stevens Advisory, we help individuals and families make informed decisions around employer stock plans, retirement distributions, taxes, and long-term financial planning. Whether you’re evaluating an ESOP payout, deciding what to do with ESPP shares, or simply want a clearer strategy moving forward, we’re always happy to be a resource.

If you’d like to talk more with our team, here’s the link to schedule a Discovery Call.

Disclaimer

This article is provided for informational and educational purposes only and should not be construed as individualized investment, tax, legal, or accounting advice. O’Keefe Stevens Advisory does not provide tax or legal advice. Readers should consult with their qualified tax professional, attorney, and financial advisor regarding their specific situation before making any decisions related to ESOPs, ESPPs, employer stock, retirement distributions, or tax strategies. Any examples provided are hypothetical and for illustrative purposes only.

Investing involves risk, including the potential loss of principal. Concentrated positions in employer stock may increase overall portfolio risk and may not be appropriate for all investors. References to tax treatment, including discussions surrounding Net Unrealized Appreciation (NUA), capital gains, and rollover strategies, are based on current federal tax laws, which are subject to change.

Disclaimer

Advisory services offered through O’Keefe Stevens Advisory, an investment adviser registered with the U.S. Securities & Exchange Commission.

No responses yet